March 18, 2024

Mike Barton10 tips to level the playing field for your next renewal

Have you “really” read your renewal exhibits? If you have, you know these are an exercise in financial engineering designed to bully or intimidate the buyer into submission (or, in this case, acceptance of the renewal).

Arcane naming conventions, unknowable methodology, and ever-changing underwriting assumptions make understanding your renewal nearly futile for even the most seasoned benefits professional.

It has become so bad, what was once titled a “Renewal Justification” has been changed to “Renewal Illustration” for regulatory purposes. The implication here is obvious. Don’t trust your renewal…

The renewal process

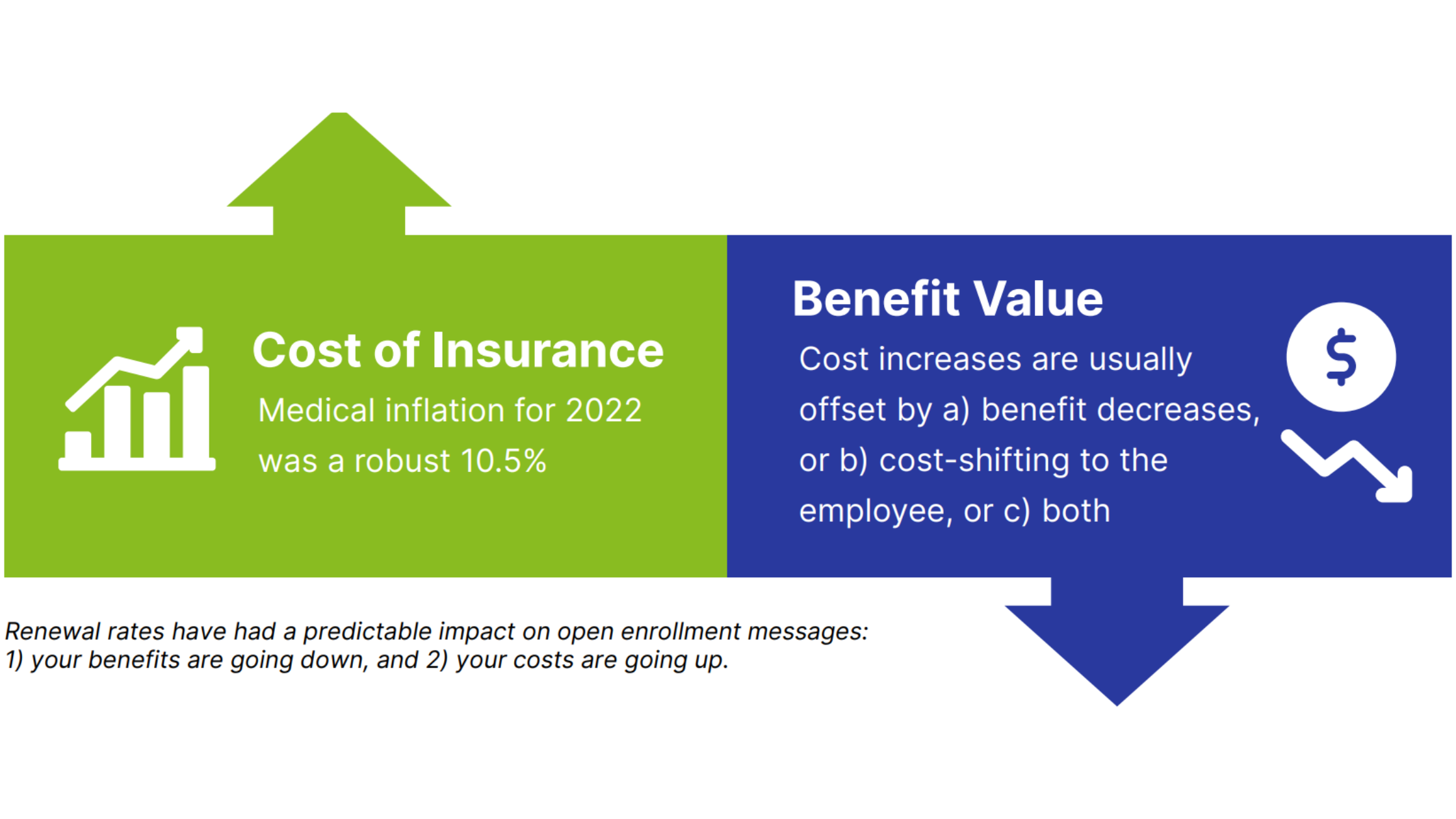

The annual renewal dance is characterized by an initial renewal salvo, followed by broker pushback, resulting in a rate compromise between the parties involved. Unfortunately, carriers anticipate this process and have built margin into almost every element of the renewal calculation. As such, the “compromise” still has excessive carrier profit in the price tag.

Even worse, medical underwriters now champion the “no bid” renewal rates. Meaning, the carrier will offer an astounding “below market” deal if the buyer agrees not to test the market. Sounds like a Ginsu Knife commercial: “but wait, there is more…” When your medical renewal process makes buying a used car seem savory and ethical, you have a problem.

Definition of a claim

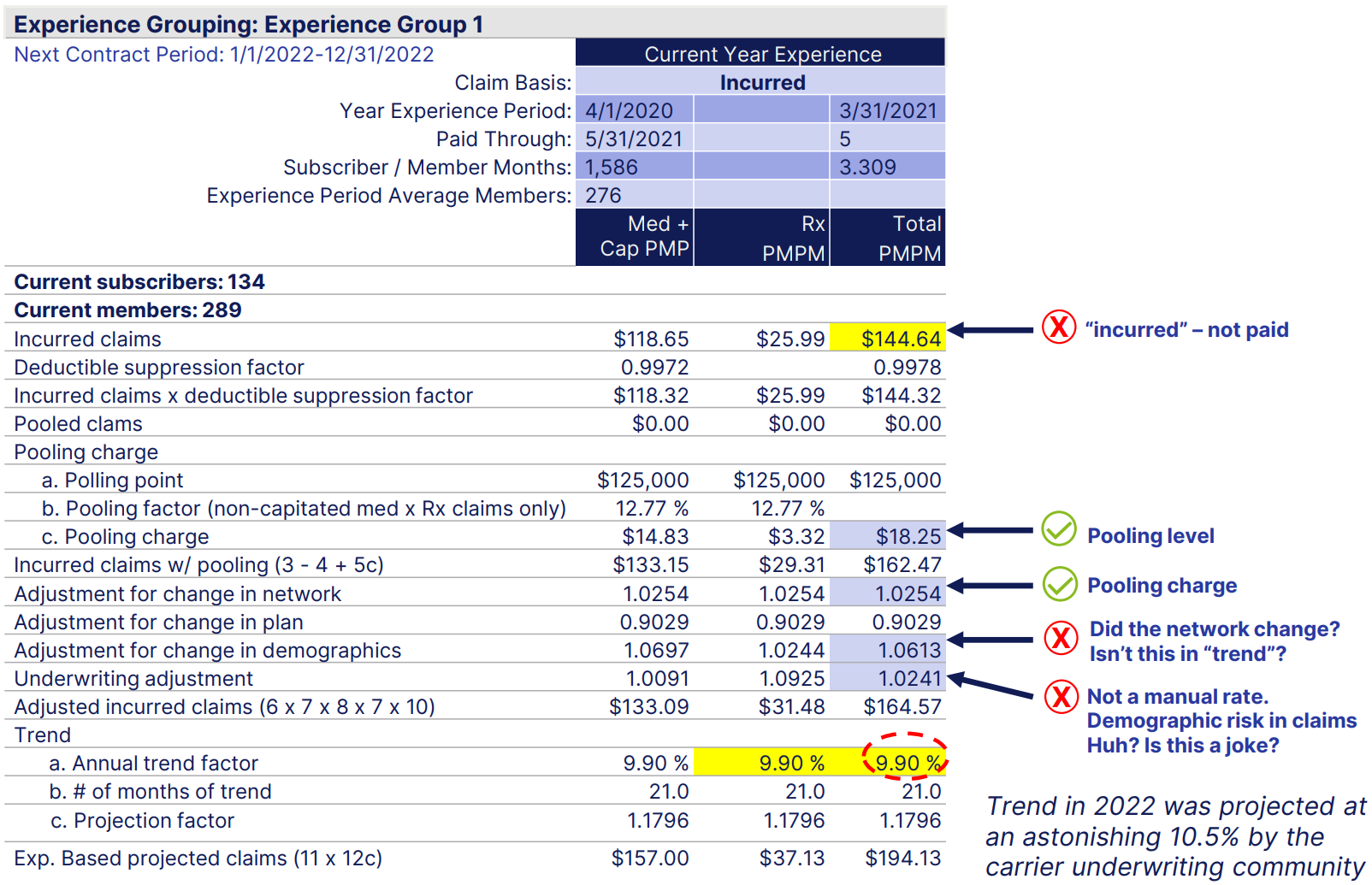

For groups greater than 100 participants, there are two pieces to your renewal. You need to understand both. The first element is your experience workup. This is an evaluation of your actual claims during the renewal period. The exhibit should be a simple depiction of cost, but you need to understand the definition of a “claim.” Is it “paid” or “incurred”? Are there charges in lieu of a claim (capitation or carrier shared savings fees)?

Blending with manual

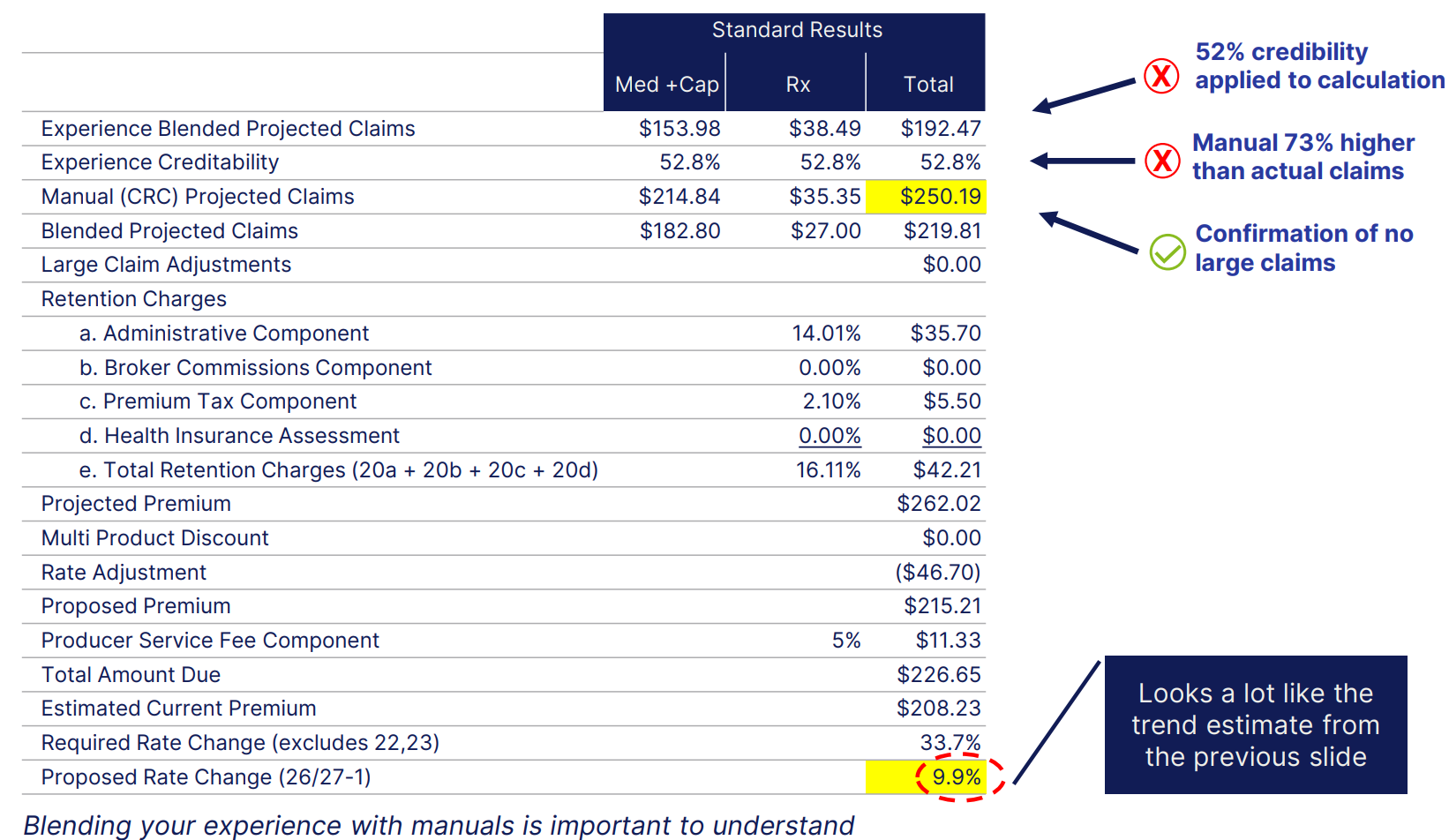

Next, the underwriter will blend your actual claims with the carrier normalized book of business results (or manual rate). Again, what should be a simple complementary exercise, is made problematic by the amount of credibility assigned you’re your experience. This is an area of carrier margin creation where manual weighting is typically used to skew renewal increases in the carriers’ favor.

While credibility is not assigned on a linear basis, you can still apply a “reasonableness test” to the weight given to your own experience in the blending process. Also, look back at previous renewals: a) blending percentage, and b) manual rate PEPM. You want to see methodology consistency period over period.

Carrier administrative charges

There is also the issue of carrier administration expense. Are your expenses calculated as a percentage or premium? Or are your expenses based on a fixed per employee per month charge (PEPM)? It costs carriers ~ $30 PEPM to administrate your plan. However, if you are charged 10% of premium for administrative expense, the cost could be more like $100 PEPM depending on premium level.

Carriers also collect significant rebates from PBMs on your Rx costs. The value of these rebates can be $20-$40 PEPM. Was this revenue used to offset or buy down your administrative expenses? Doubtful.

Renewal calculation methodology

Your renewal is actually two renewals for groups with less than 400 employees on the plan. The carrier will provide an experience-based renewal as well as an age/gender plan design adjusted manual work-up. The two are blended in proportion to the credibility assigned to the buyers own experience (with the compliment going to the manual).

There are a lot of moving parts in the calculation. To avoid confusion or misdirection, we recommend you understand your own piece of the equation: the experience-based renewal calculation. In short, the renewal formula can be articulated as:

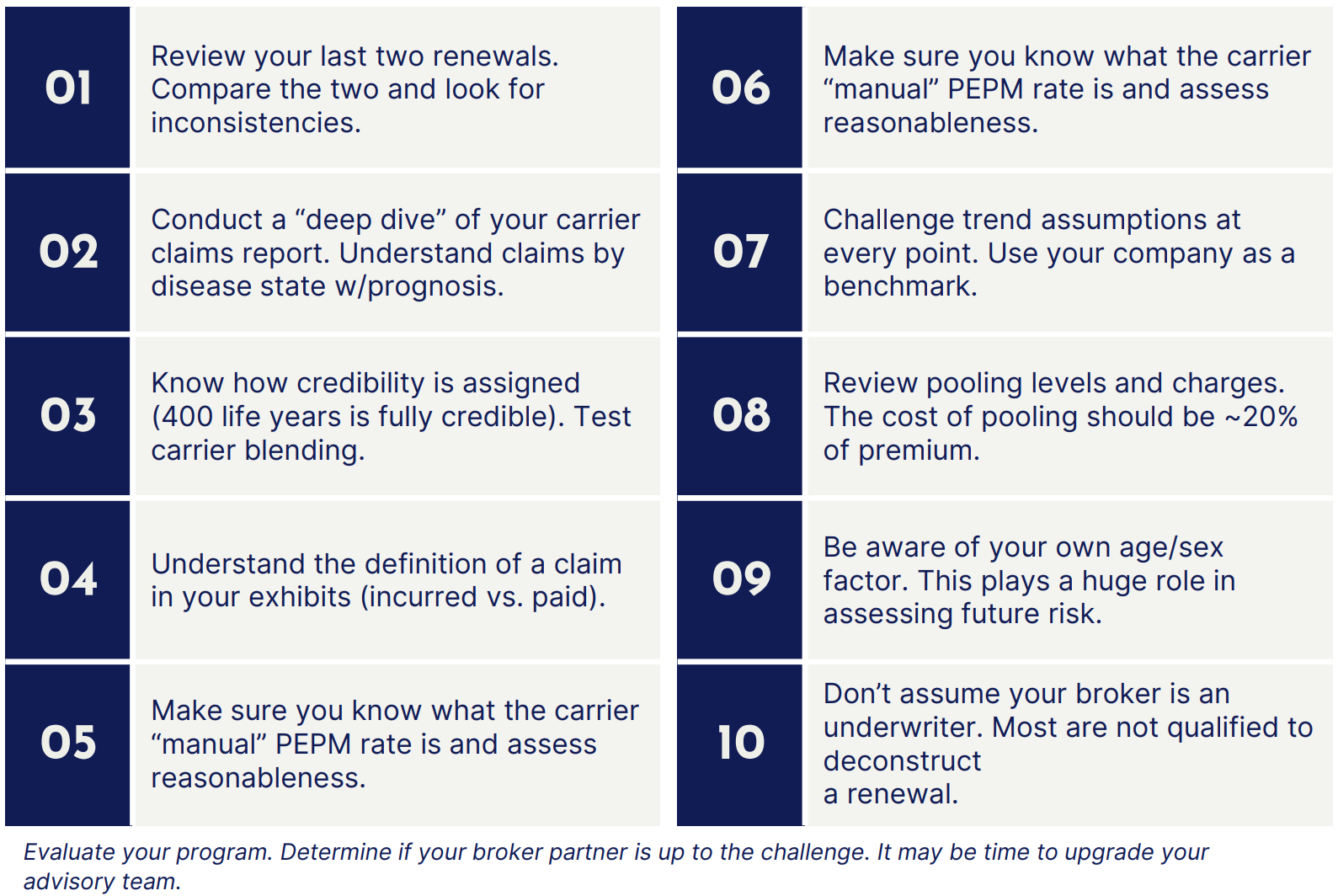

10 tips to level the playing field at your next renewal

First, don’t assume your carrier underwriter “has your back.” Medical carriers operate for one purpose: to maximize underwriting gain. What used to be a straightforward renewal justification has become a charade.

The only assumption you can make about your renewal, is that the “illustration” (if you even get one), bears little resemblance to the truth — and may only be directionally accurate.

Given this, and the tripling of costs since the ’90s, most employers with greater than 100 participants may be better off self-funding (or at least performing an honest feasibility study forecasted with confidence bands over a 5-year period).

Understanding the renewal underwriting process will help you level the playing field when you do battle with the underwriter at your next renewal. The 10 tips below represent important steps you need to take to decode your medical

renewal and produce an optimized outcome.

This update is not intended to be exhaustive, nor should any discussion or opinion be construed as legal advice. Readers should contact legal counsel for legal advice. All rights reserved.